In diesem Artikel

Transitorische Aktiven und Passiven (Rechnungsabgrenzungen) sind Abschlussbuchungen am Ende des Geschäftsjahres. Sie dienen dazu, das Prinzip der periodengerechten Rechnungslegung anzuwenden. Dabei werden Aufwände und Erträge dem Geschäftsjahr zugeordnet, zu dem sie wirtschaftlich gehören – unabhängig vom Zeitpunkt der Zahlung oder des Zahlungseingangs.

Achtung

Rechnungsabgrenzungen betreffen nicht einfach unbezahlte Rechnungen oder noch nicht eingegangene Zahlungen. Es handelt sich vielmehr um buchhalterische Abgrenzungen, die notwendig sind, um den Periodenerfolg eines Geschäftsjahres korrekt zu ermitteln.

Unterschied zwischen transitorischen Aktiven und Passiven (Rechnungsabgrenzungen)

Am Ende des Geschäftsjahres können zwei Situationen auftreten:

- Aufwände oder Erträge sind bereits entstanden, aber noch nicht verbucht → Rechnungsabgrenzung (TA oder TP)

- Aufwände oder Erträge wurden bereits verbucht, betreffen jedoch ganz oder teilweise das nächste Geschäftsjahr → Rechnungsabgrenzung (TA oder TP)

Einfache Regel

- Rechnungsabgrenzungen (transitorische Aktiven und Passiven) erfassen fehlende Aufwände oder Erträge

- und verschieben bereits verbuchte Aufwände oder Erträge, die das nächste Geschäftsjahr betreffen.

Aktive und passive Rechnungsabgrenzungen

Rechnungsabgrenzungen betreffen Aufwände und Erträge, die wirtschaftlich in ein Geschäftsjahr gehören, deren Zahlung oder Einnahme jedoch in einem anderen Geschäftsjahr erfolgt.

Man unterscheidet zwei Arten:

- Aktive Rechnungsabgrenzungen (TA) → noch zu erhaltende Erträge

- Passive Rechnungsabgrenzungen (TP) → noch zu erhaltende Erträge

Der Aufwand oder Ertrag gehört vollständig zum laufenden Geschäftsjahr, wurde jedoch noch nicht bezahlt oder vereinnahmt.

Rechnungsabgrenzungen für vorausbezahlte und vorauserhaltene Beträge

Diese Rechnungsabgrenzungen betreffen Aufwände und Erträge, die bereits verbucht wurden, jedoch ganz oder teilweise das nächste Geschäftsjahr betreffen.

Man unterscheidet:

- Aktive Rechnungsabgrenzungen (TA) → verschieben einen Teil eines bereits verbuchten Aufwands ins nächste Geschäftsjahr

- Passive Rechnungsabgrenzungen (TP) → verschieben einen Teil eines bereits verbuchten Ertrags ins nächste Geschäftsjahr

Rechnungsabgrenzungen in der Struktur des Kontenplans von Banana Buchhaltung

Rechnungsabgrenzungen werden durch normale Buchungen in der Tabelle Buchungen erfasst. Dabei werden spezifische Bilanzkonten im Kontenplan verwendet.

Diese Konten sind in den folgenden Untergruppen aufgeführt:

Umlaufvermögen

- 1300 Aktive Rechnungsabgrenzungen (im Voraus bezahlte Aufwände)

- 1301 Erträge einzuziehen (noch nicht erhaltener Ertrag)

Kurzfristiges Fremdkapital

- 2300 Noch nicht bezahlte Aufwände

- 2301 Im Voraus erhaltene Erträge

Im Folgenden wird anhand von Beispielen erläutert, wie aktive und passive Rechnungsabgrenzungen in der Tabelle Buchungen von Banana Buchhaltung verbucht werden.

Buchhaltungsmethode und Rechnungsabgrenzungen

- Beim Kompetenzprinzip (nach vereinbarten Entgelten) werden ausgestellte oder erhaltene Rechnungen direkt auf den Konten Kunden oder Lieferanten verbucht und erscheinen als offene Posten.

- Beim Kassenprinzip (nach vereinnahmten Entgelten) sind am Jahresende Rechnungsabgrenzungen notwendig, um bereits entstandene Aufwände und Erträge zu erfassen, die noch nicht bezahlt oder eingezogen wurden.

- Bei der gemischten Methode (Kassen-/Kompetenzprinzip) wird jeweils die Lösung angewendet, die am besten zur verwendeten Buchungsmethode passt.

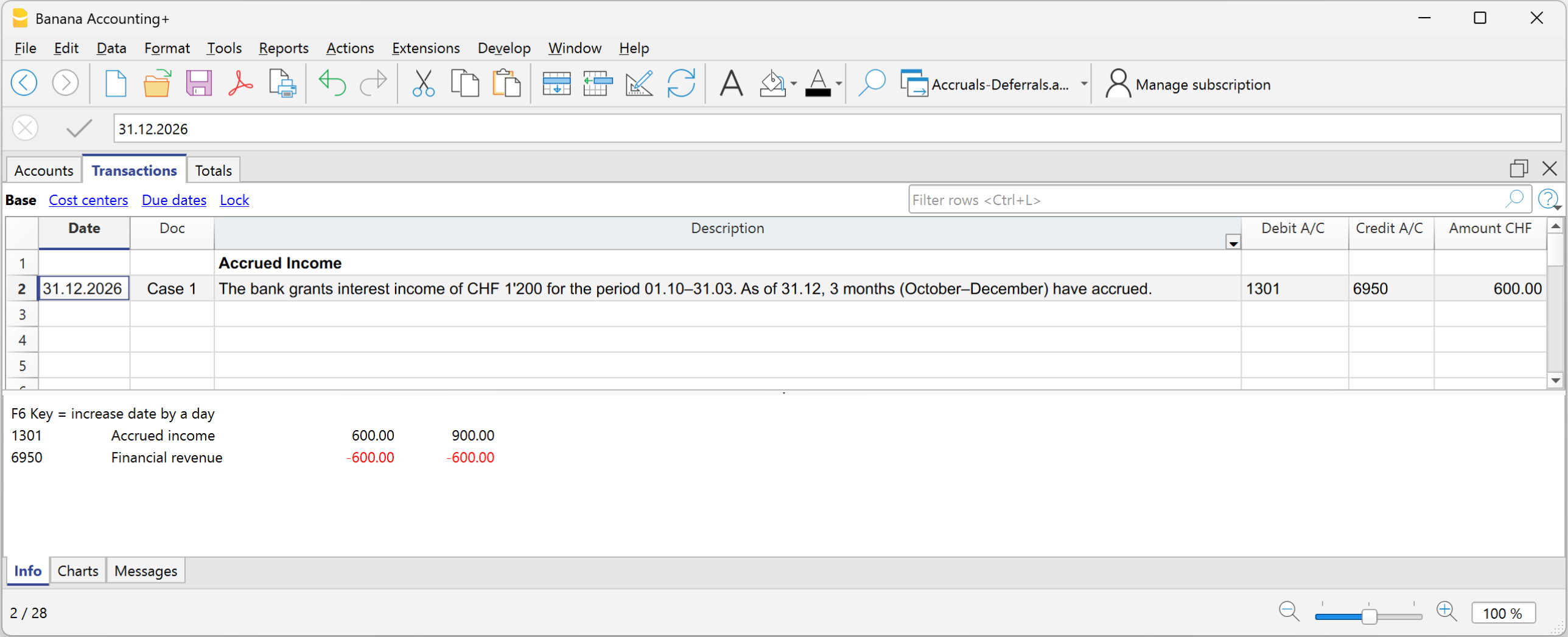

Fall 1 – Aktive Abgrenzung (noch einzuziehende Erträge)

Beispiel: Die Bank schreibt Aktivzinsen von CHF 1’200.00 für den Zeitraum 01.10.–31.03. gut. Bis zum 31.12. sind 3 Monate aufgelaufen (Oktober–Dezember).

Anteil des laufenden Jahres

- CHF 1’200 ÷ 6 Monate × 3 Monate = CHF 600.00

Buchung am 31.12.

- Soll: 1301 Erträge einzuziehen CHF 600.00

- Haben: 6950 Aktivzinsen CHF 600.00

In der Erfolgsrechnung werden CHF 600.00 als Ertrag des laufenden Geschäftsjahres ausgewiesen. In der Bilanz erscheint eine aktive Rechnungsabgrenzung für die aufgelaufenen, aber noch nicht erhaltenen Zinsen.

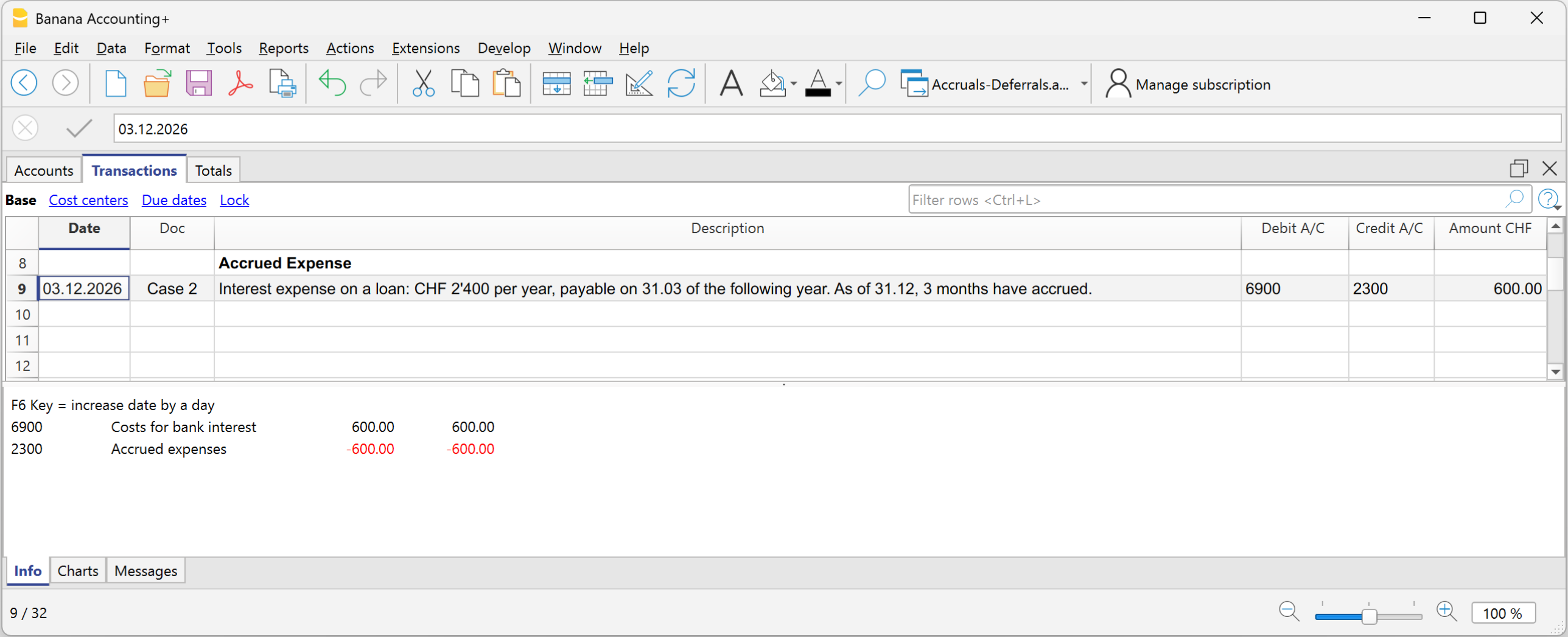

Fall 2 – Passive Abgrenzung (noch zu zahlende Aufwände)

Beispiel: Passivzinsen auf ein Darlehen: CHF 2’400.00 pro Jahr, zahlbar am 31.03. des folgenden Jahres.

Bis zum 31.12. sind 3 Monate aufgelaufen.

Anteil des laufenden Jahres

CHF 2’400 ÷ 12 Monate × 3 Monate = CHF 600.00

Buchung am 31.12.

- Soll: 6900 Passivzinsen CHF 600.00

- Haben: 2300 Noch zu zahlende Aufwände (Verbindlichkeit) CHF 600.00

In der Erfolgsrechnung werden CHF 600.00 als Aufwand des laufenden Geschäftsjahres ausgewiesen. In der Bilanz erscheint eine passive Rechnungsabgrenzung für die aufgelaufenen, aber noch nicht bezahlten Zinsen.

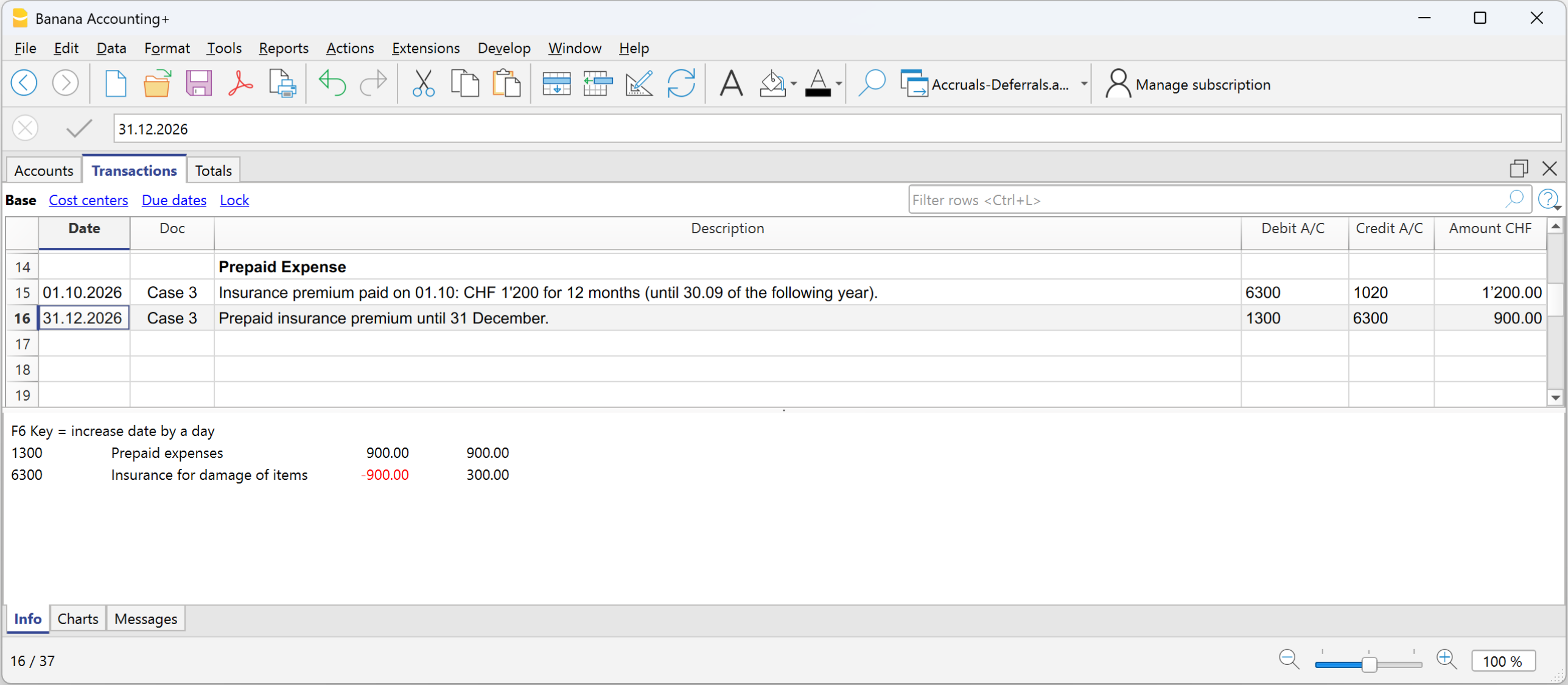

Fall 3 – Aktive Rechnungsabgrenzung (im Voraus bezahlte Aufwände)

Beispiel: Versicherungsprämie von CHF 1’200.00 für 12 Monate, bezahlt für den Zeitraum 01.10. bis 30.09. des folgenden Geschäftsjahres.

Zeitraum des laufenden Jahres

Oktober–Dezember = 3 Monate

Anteil des laufenden Jahres

CHF 1’200 ÷ 12 Monate × 3 Monate = CHF 300.00

Anteil des folgenden Jahres

CHF 1’200 − CHF 300 = CHF 900.00

Buchung am 31.12.

- Soll: 1300 Aktive Rechnungsabgrenzungen CHF 900.00

- Haben: Versicherungsaufwand CHF 900.00

In der Erfolgsrechnung verbleibt ein Aufwand von CHF 300.00 für das laufende Geschäftsjahr. In der Bilanz erscheinen CHF 900.00 als aktive Rechnungsabgrenzung, da dieser Anteil der Versicherungsprämie das folgende Geschäftsjahr betrifft.

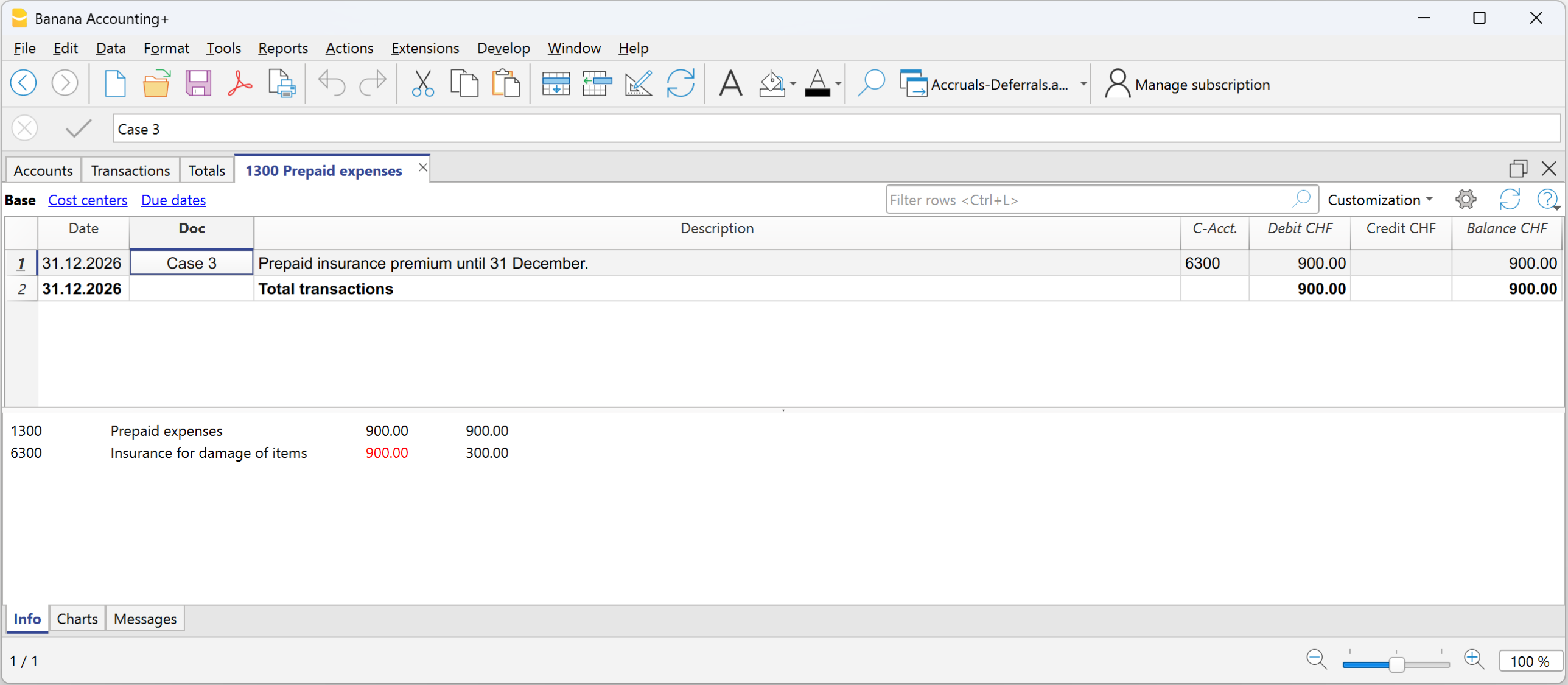

Auszug aus dem Konto 1300 Aktive Rechnungsabgrenzungen

Auszug aus dem Konto 6300 Versicherungsaufwand

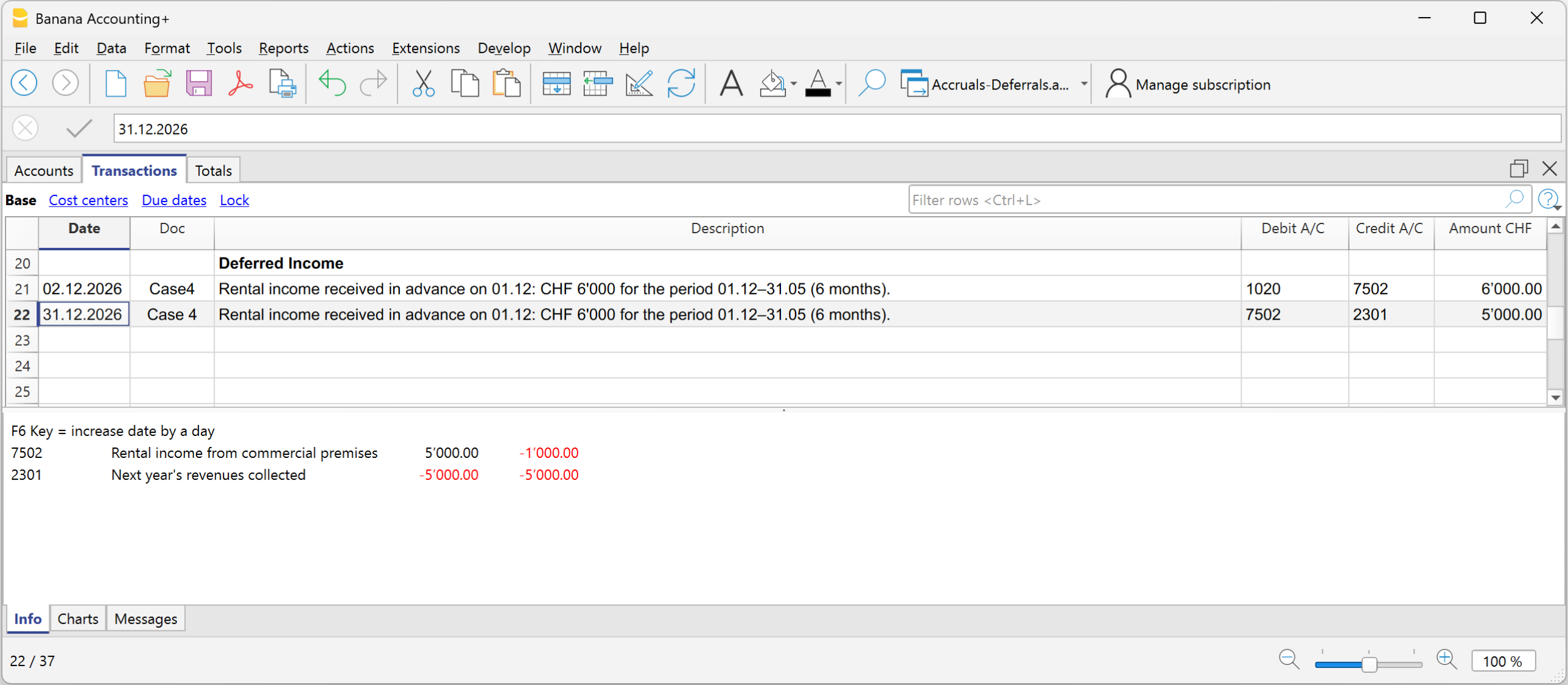

Fall 4 - Passive Rechnungsabgrenzung (im Voraus erhaltene Erträge)

Beispiel: Halbjährliche Miete von CHF 6’000.00, im Voraus am 01.12. erhalten, für den Zeitraum 01.12.–31.05.

Monatlicher Anteil

CHF 6’000 ÷ 6 Monate = CHF 1’000.00 pro Monat

Anteil des laufenden Jahres

Dezember = CHF 1’000.00

Anteil des folgenden Jahres

5 Monate = CHF 5’000.00

Anfangsbuchung

- Soll: Bank CHF 6’000.00

- Haben: Mieterträge CHF 6’000.00

Buchung am 31.12.

- Soll: Mieterträge CHF 5’000.00

- Haben: 2301 Passive Rechnungsabgrenzungen (im Voraus erhaltene Erträge) CHF 5’000.00

In der Erfolgsrechnung wird ein Ertrag von CHF 1’000.00 für das laufende Geschäftsjahr ausgewiesen. In der Bilanz erscheinen CHF 5’000.00 als passive Rechnungsabgrenzung, da dieser Betrag das folgende Geschäftsjahr betrifft und eine Verpflichtung darstellt.

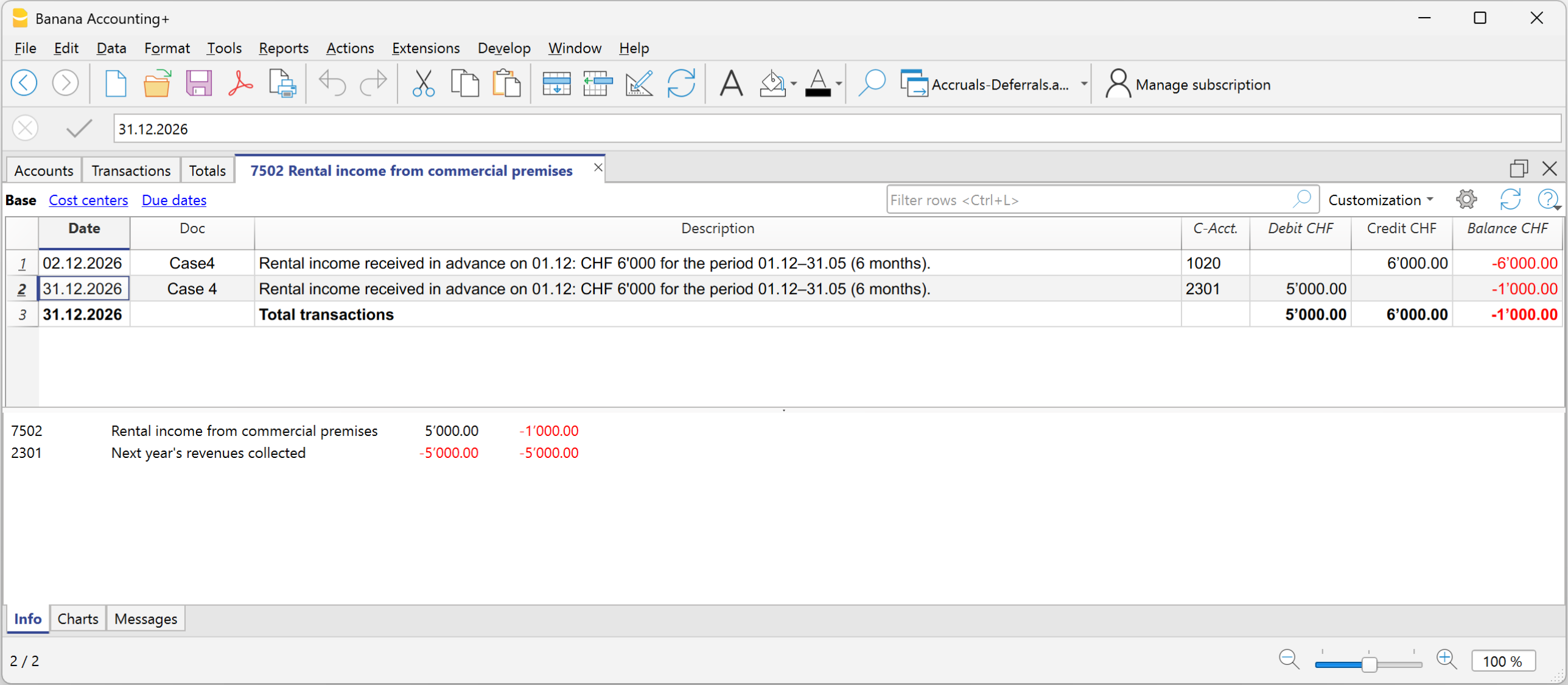

Auszug aus dem Konto 7502 Mieterträge

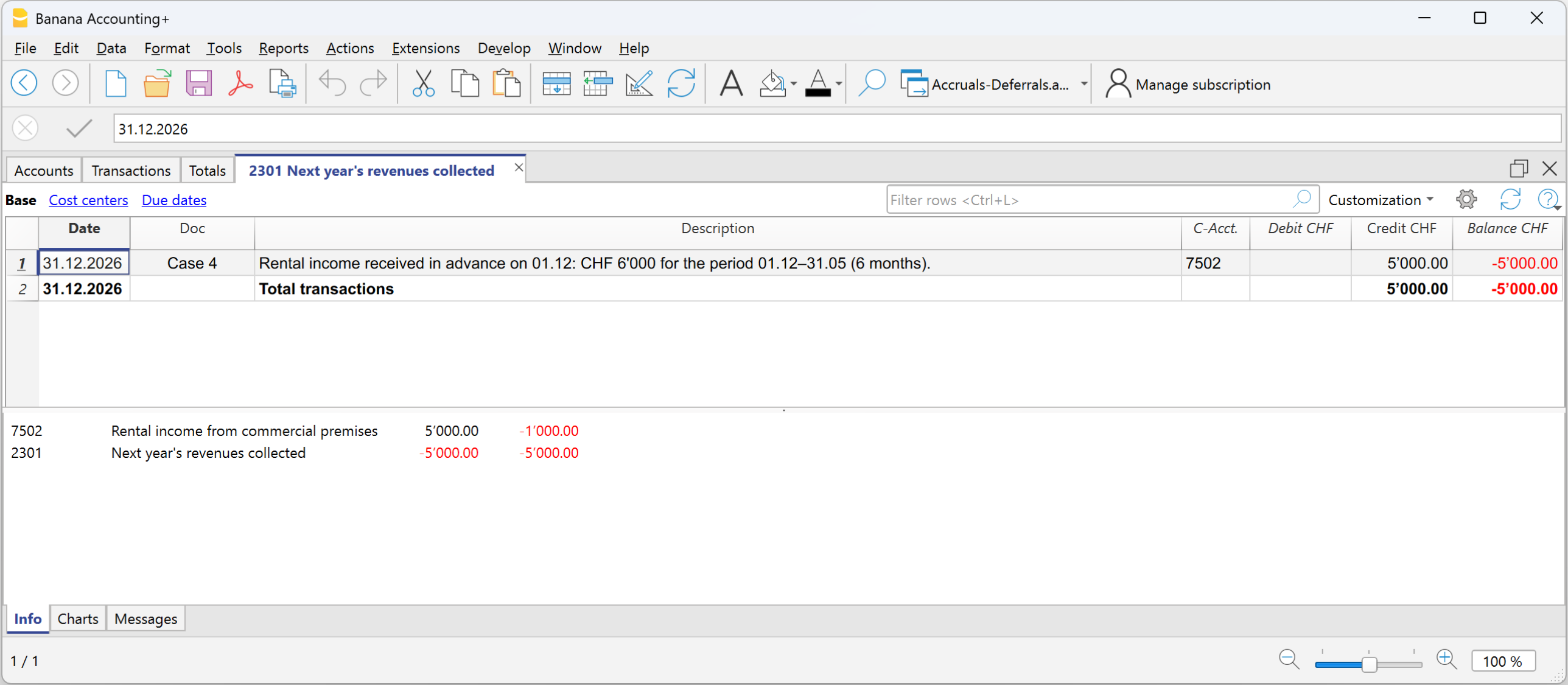

Auszug aus dem Konto 2301 Passive Rechnungsabgrenzungen (im Voraus erhaltene Erträge)

Auflösung im folgenden Geschäftsjahr

Zu Beginn des neuen Geschäftsjahres werden aktive und passive Rechnungsabgrenzungen wieder aufgelöst.

Für die Auflösung werden dieselben Konten verwendet wie bei der Bildung der Abgrenzungen:

- die Konten der Rechnungsabgrenzungen sowie die entsprechenden Aufwands- und Ertragskonten werden durch eine Gegenbuchung ausgeglichen.

- Alternativ kann die Auflösung auch zum Zeitpunkt der Zahlung oder des Zahlungseingangs erfolgen.

Die Auflösung ist notwendig, um die Konten der aktiven und passiven Rechnungsabgrenzungen zu schliessen.

Kurz zusammengefasst:

Abgrenzungen ergänzen, was noch fehlt; Rechnungsabgrenzungen verschieben, was im Voraus verbucht wurde.