In this article

There are two methods, established by the Federal Tax Administration, for the collection of the Value Added Tax (VAT):

- Turnover method - the determination of the VAT amount occurs when the suppliers' invoices are received and when invoices are issued to customers. This method involves managing both customers and suppliers.

- Method based on cash received - the determination of the VAT occurs when customer invoices are collected and supplier invoices are paid.

Recording Invoices with VAT on Cash Received

- Throughout the fiscal year, customers and suppliers should not be recorded. Only at the year-end are open items recognized, namely, invoices from customers and suppliers that remain uncollected and unpaid, respectively, as of December 31st.

- Costs and revenues must be recorded at the time of payment or collection.

- The VAT code must be entered on the same line as the cost or revenue.

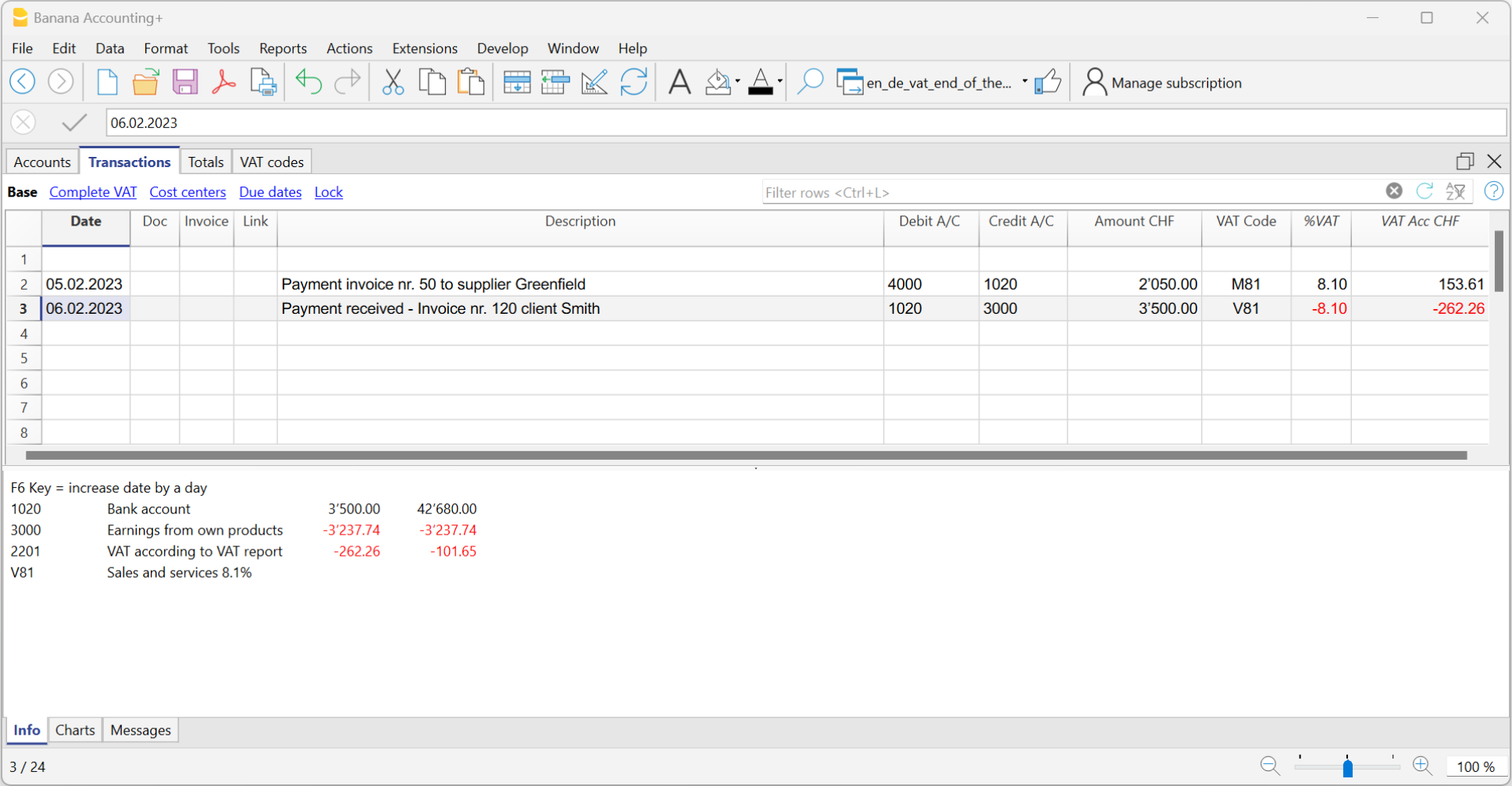

Example showing how to enter transactions during the year

Customers and Suppliers with VAT on Cash Received

If you want to equally manage customers/suppliers, you can use the profit and cost centers. In this case, the clients/suppliers management remains separated from the Balance Sheet.

As for the transitory assets or liabilities (invoices issued for income/expenses, but not yet received or paid), only at the end of the year, carrying forward of the outstanding invoices of suppliers and clients is allowed. These issues are defined by the VAT regulations (Instructions for VAT, at marginal number 964, page 217).

Starting from here, we present you one of the possible solutions:

Transitory assets or liabilities as at the end of the year

At the end of the year, in order to exactly establish the profit or the loss of the accounting year, one needs to enter the transitory assets or liabilities:

- Invoices issued to customers but not yet collected.

- Invoices received from suppliers but not yet paid.

- Work in progress, to be collected or paid in the following year.

When recording suspense of open items, caution should be taken not to include the VAT code on costs and revenues. Recoverable VAT and due VAT should be reported in the VAT statement for the first quarter of the following year.

The accounts for transitory invoices

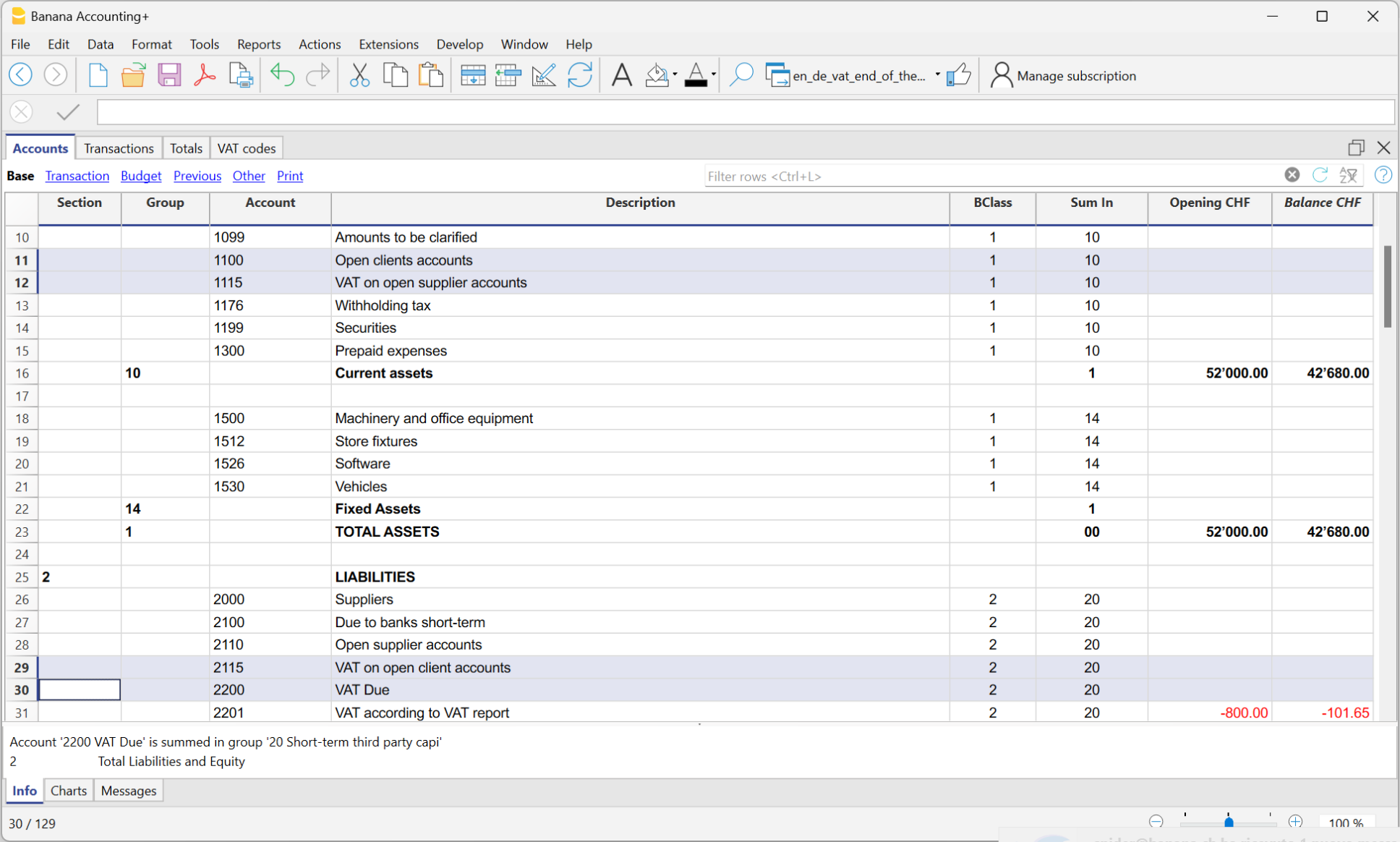

To capture only the net portion of costs and revenues (excluding VAT) at the end of the year and record it correctly, it is necessary to open the following accounts:

In the Assets and Liabilities

- In the Assets, open the account "Open client accounts"

- In the Liabilities, open the account "VAT on open client accounts"

- In the Liabilities, open the account "Open supplier accounts"

- In the Assets, open the account "VAT on open supplier accounts"

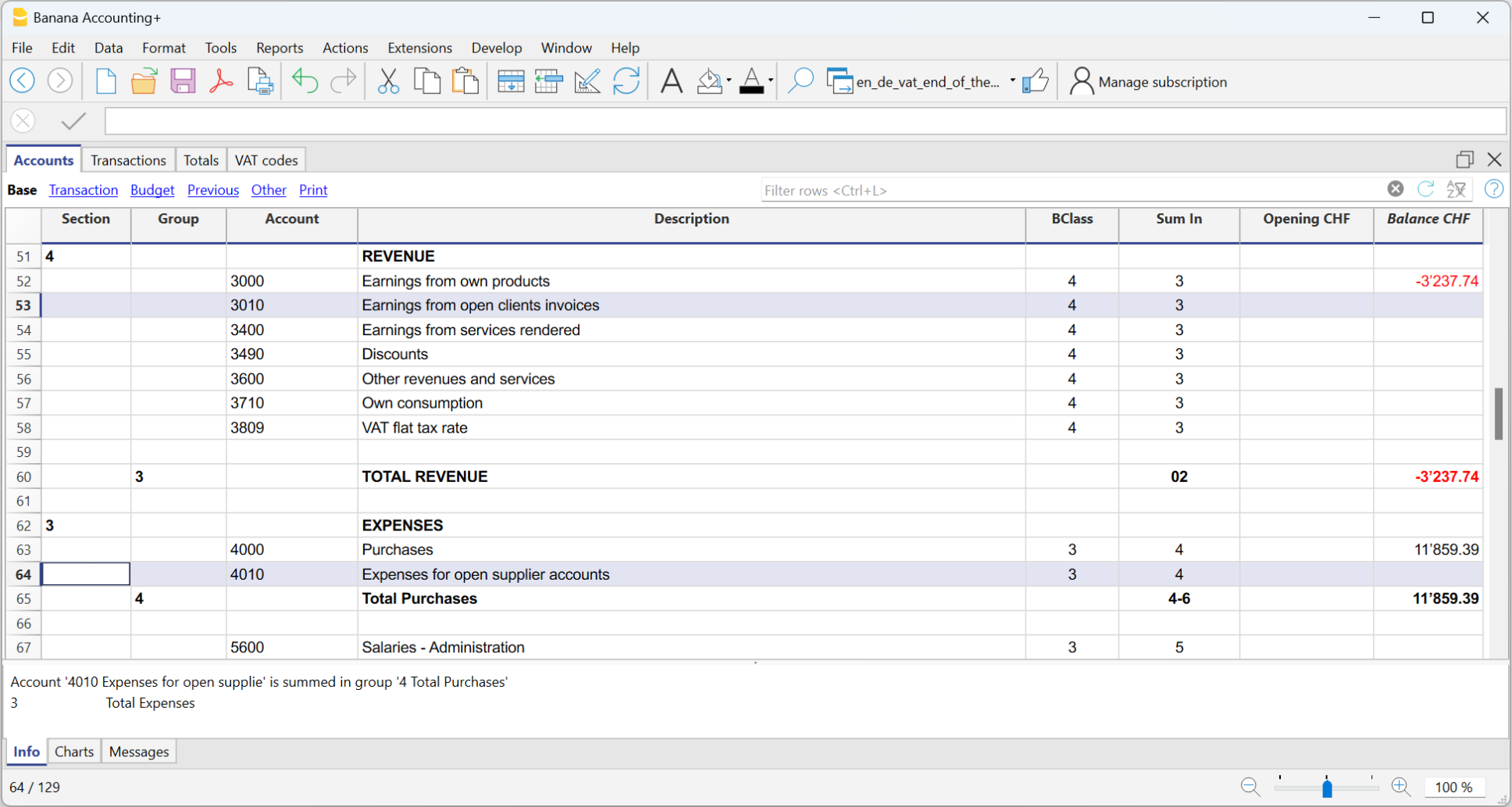

In the expenses and income

In the income statement, open the following accounts

- In the expenses, open the account "Expenses for open supplier accounts"

- In the income, open the account "Income for open client invoices"

How to register transitory supplier invoices

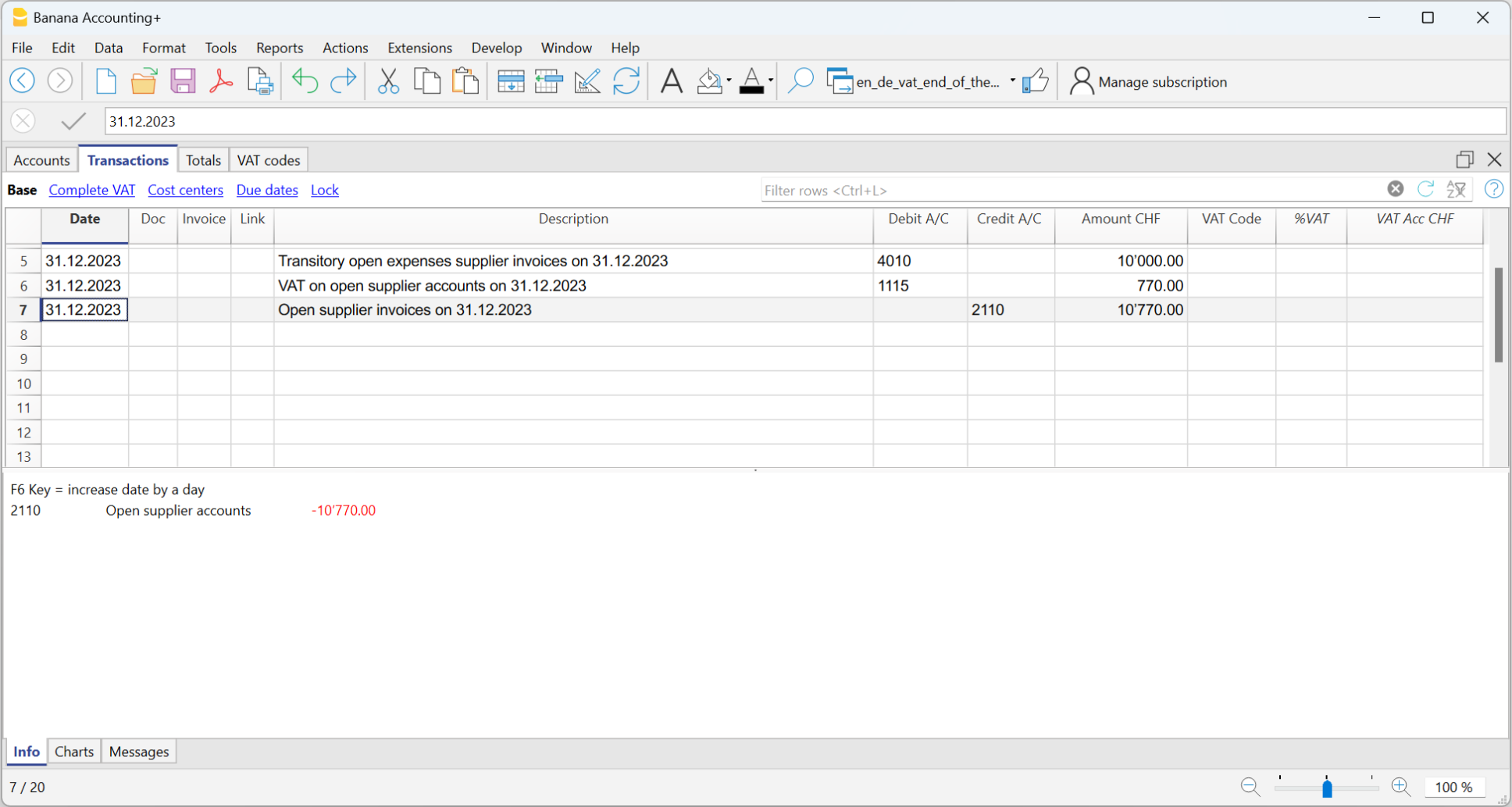

At the end of the year, open invoices from suppliers received as of December 31 are recorded as follows:

- Enter in the Debit column on the account Expenses for open supplier accounts the expense without VAT in the Amount column, without VAT code.

- Enter in Debit column in the following row, on the account VAT on open supplier accounts and in the Amount column,the recoverable VAT amount.

- Enter in Credit column in the following row, on the account Open supplier accounts and in the Amount column the total amount (VAT included)

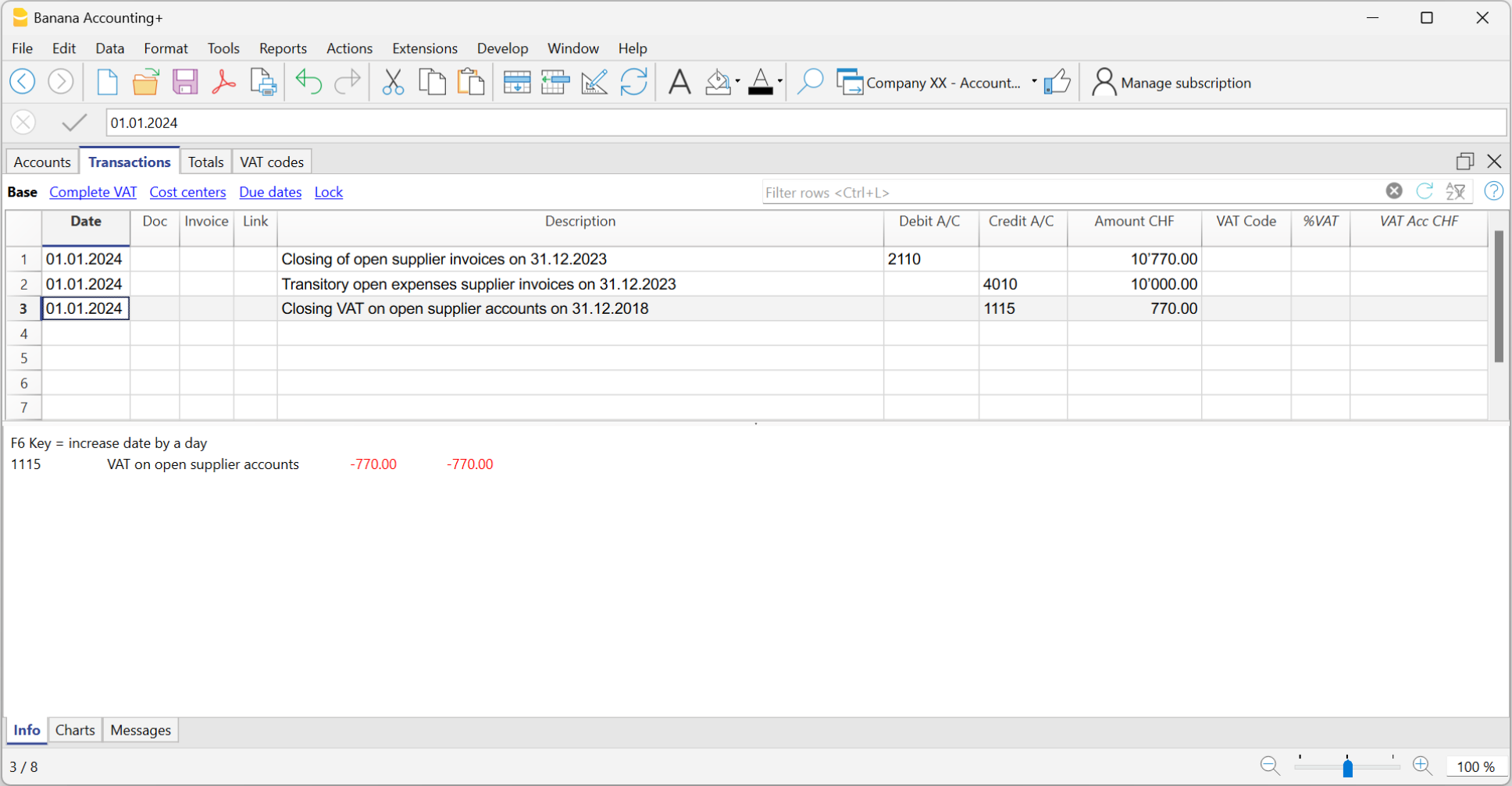

Closing transitory invoices

To close open items on January 1st of the following year, reverse the transactions made on December 31st as follows:

- Enter in the Debit column, on the account Open suppliers accounts the total amount (VAT included).

- Enter in the Credit column on the following row, the Transitory open expenses supplier invoices and in the Amount column the expense without VAT, without VAT code.

- Enter in the Credit column on the following row, the account VAT on open supplier accounts and in the Amount column the recoverable VAT amount.

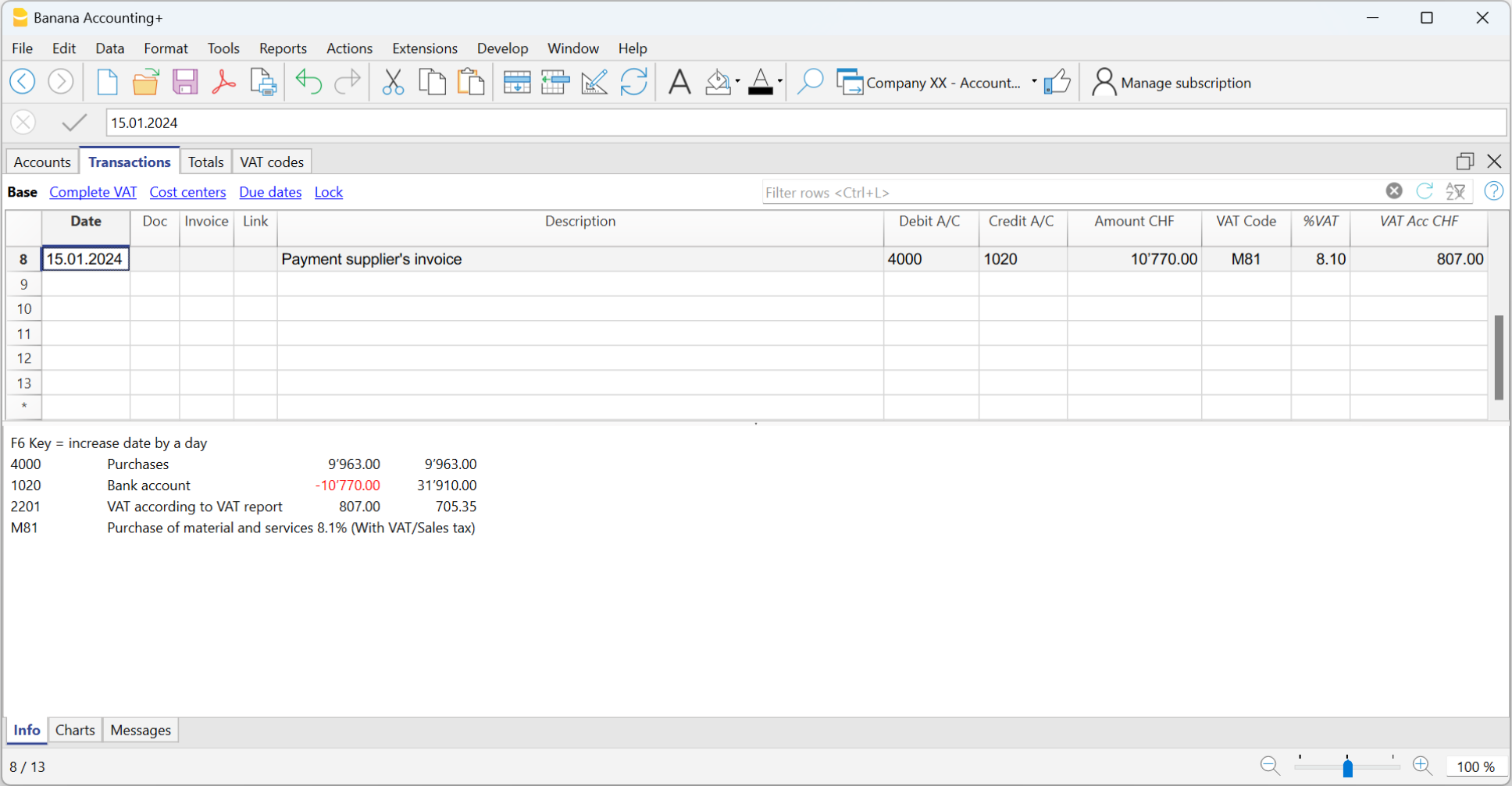

When the supplier's invoice is paid, the user has to enter the transaction as shown in the example at the beginning of this page, by inserting the VAT code as usual.

How to register the transitory client invoices

For the transitory client invoices, the same procedure needs to be applied, by entering on the preconfigured accounts related to the open client accounts.